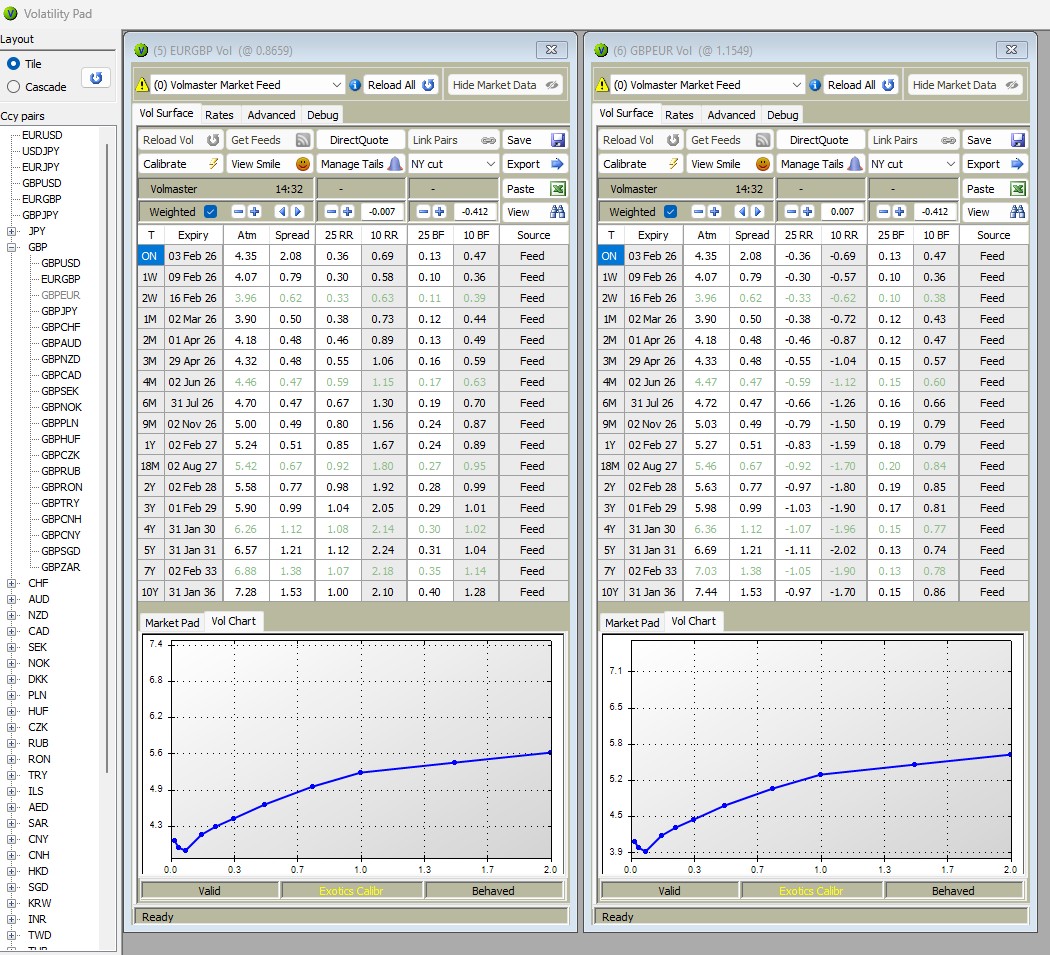

Volmaster is now managing flipped twin ccypairs

Volmaster FX is now managing any illiquid reciprocal pair (such as GBP/EUR) as a pair on its own, but with a strong link to its principal pair (EUR/GBP).

In the old times all the way up to 1st generation exotics, a basic approach of taking reciprocals of strikes and other similar provisions would have been sufficient to price an instrument based on a flipped twin. However, such a simplicistic approach does not work for 2nd generation of exotics or structured products. For example, the target of an FX TARF expressed in Big Figures is a linear measure and cannot be 'flipped' in any meaningful way. As a result, Volmaster FX has taken the approach to keep a principal pair (EUR/GBP) and its flipped twin (GBP/EUR) as separate pairs, so that any instrument, no matter how complex, can be priced and revalued correctly.

In order to enforce consistency between the principal pair and the flipped twin pair, any update on the volatility surface of the former will automatically compute and update the equivalent volatility surface of the latter. The calculation is not trivial and in general it does not lead to identical surfaces - save for an opposite sign of the risk reversals. On the contrary, the twin surfaces will be rather different (especially in terms of the long-term butterfly), mainly due to distorsive market conventions. But no matter the conventions, the two surfaces will produce exactly the same prices for the same instruments, whether priced on the principal pair or on its flipped twin.

All the high-end features of Volmaster, such as Traffic / RFQ, automatic updates, weights management, API integrations, etc. work seamlessly and consistently for flipped twins too.